The international scientific and analytical, reviewed, printing and electronic journal of Paata Gugushvili Institute of Economics of Ivane Javakhishvili Tbilisi State University

Blockchain technologies for managing public debt

10.36172/EKONOMISTI.2024.XX.01.Givi.Bedianashvili/Zviad.Gabroshvili

Annotation. The study presents the application of blockchain technologies in the direction of public debt management. Existing models for debt management are mentioned, such as the debt, investment, growth model and the debt, investment, growth and natural resources model. An important component for achieving sustainability, the use of blockchain technology for increasing the efficiency of state investments, which implies the transparency of investments, is presented. The study showed how the government should use blockchain technology to make investments more efficient and transparent, which could reduce the likelihood of an explosive debt problem. The paper also discusses how the state can find resources through blockchain technology and, in certain cases, reduce the public debt based on the emergence of new reserves. The risks of using this technology are also shown, which can cause significant problems in the direction of the stability of the state economy.

Keywords: blockchain technologies, public debt management, investment transparency

Introduction

Issues related to public debt management are of great interest to the society of any country. The size of the public debt, issues directly related to management and annual growth rates are naturally the object of special attention of scientific-research publications.

There are few scientific publications about the use of blockchain technologies in the process of public debt management (see, for example, MacDonald, 2022). However, in recent years, publications have appeared on the problems of using blockchain technologies in other areas of society (Ahmed, A., 2018; Akins et al, 2013; Casino et al, 2019; Douglas et al, 2015; Kim & Laskowski, 2016; Ko & Verity, 2016; McKinseyCompany, 2016; Sichinava & Maghradze, 2023; Swan, 2017) . Their analysis shows that the potential and possible area of application of blockchain technologies is quite diverse (Figure 1).

Figure 1. Areas of application of blockchain technologies

Source: Casino et al, 2019.

Recently, the problem of public debt has been acute worldwide. Different models have been created to solve public debt problem, listing a few of them will show us how large-scale the mentioned task is:

- Can exogenous growth in government spending be financed by tax increases or borrowing? (Barro, 1979)

- Relationship between debt, investment and economic growth: Debt, Investment, Growth (hereinafter DIG) model. (Buffie et al, 2012).

- The relationship between public debt, investments and economic growth in countries with rich resources: Debt, investment, growth, natural resources (hereinafter DIGNAR) model. (Berg et al, 2013)

The research of the public debt in Georgia is one of the important issues on which many interesting papers have been written (Bedianashvili & Kokhreidze, 2023; Charaia & Papava, 2021).

As for blockchain technologies, they have made a significant change in the world economy. Various cryptocurrencies have been introduced, which have different features and capabilities. In some blockchains, if a limited amount of cryptocurrency can be issued, in others this restriction is removed.

In the mentioned paper, we review the possibilities of using blockchain technologies in the direction of public debt.

Blockchain review

In 1998 computer scientist Nick Szabo created method for decentralized digital currency, which he called ‘bit gold’. He also created the concept of smart contract. This is one of the early developments towards blockchain technology.

After that, in 2008 anonymous person or person group named Satoshi Nakamoto invented first cryptocurrency bitcoin, which was using blockchain technology. This technology solved double-spending problem in peer-to-peer network. In cryptocurrency Blockchain contains the records of all transactions in the system. It also contains genesis block where certain amount of cryptocurrency is issued by the creator of that currency. The price of bitcoin in 2017 rapidly increased and so the popularity of the Blockchain technology did.

Blockchain technology today is used for storing data, using smart contracts and for cryptocurrencies. Some implementations of Blockchain are the way of transparency.

There are more than 25 000 cryptocurrencies in the world of February 2024. Some of them have very high market capitalization and are the good source of income for investors, but some of them caused significant loses.

Blockchain technology for public dept efficiency

Blockchain itself can be used to improve the efficiency of public debt. In the DIG and DIGNAR models, one of the key equations linking public capital and investment is given in the first equation.

ktg = (1 — δ)kgt-1 + ε * itg (1)

In the mentioned equation, ktg is public capital in time period t, δ is depreciation, itg is public investment, and ε is the efficiency of public investment. Funding for public investment can come from both savings and debt. In general, the parameter ε varies between zero and one and shows how much of the public investment has become productive capital. A low value of the mentioned parameter can be caused by both governance and corruption deficiencies, as well as unexpected cost overruns. A certain value of the ε parameter in a certain period can lead to an explosive debt problem, with negative economic or social consequences.

In order for the effectiveness of public investment to be high, it is important for a specific investment project to be economically observable. This traceability can be achieved with Blockchain technology, with the help of which the company implementing the project can make the necessary transfers (it is necessary to integrate the mentioned blockchain with the financial system), whether it is for the purchase of specific products or for payment of labor. Subsequently, these transfers can be analyzed by chain analysis and the results can be drawn:

- What part of the investment was used for wages and how many people were paid. Whether a particular worker's salary matches the average or median salary in the market or how far the salary is from the average or median.

- The executor of a particular project may require goods and services from another organization. It will be given how much money was transferred to another organization and for what purpose. This will determine how effective and efficient the mentioned expenditure was.

- A unified database of the costs of specific projects will be created, which will be used to evaluate the effectiveness of projects by statistical methods and it will be usable for forecasting in the future.

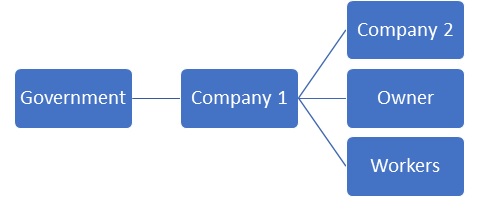

Figure 2 illustrates the flow of funds before using blockchain technology. Here government gives funds to company 1, company 1 buys goods and services from company 2, pays wages to workers and pays dividends to owner. If the links between economic agents are not controlled sufficiently in state-funded project, the risks of corruption and inefficiencies increase. As for debt in DIG model, if the links are not controlled, then the efficiency of public investment decreases, which may cause exploding debt problem.

Figure 2. Flow of funds before Blockchain technology

Source: Compiled by the authors

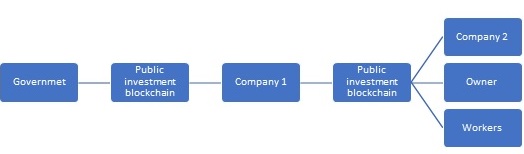

Figure 3 illustrates the flow of funds after using blockchain technology. Here government send funds to company 1 using some blockchain technology, in our example let’s call it `Public investment blockchain`. If the company wants to buy goods and services, pay wage and dividends, the working scheme works like this:

- Company 1 wants to buy goods and services from company 2, every transaction with appropriate document is recorded in public investment blockchain;

- Company 1 pays wages to workers, here each wage to each person is recorded in public investemnt blockchain with appropriate document;

- Company 1 pays dividends to its owners, here each paid dividend is recorded in the public investment blockchain with appropriate document.

Figure 3. Flow of funds after using blockchain technology

Source: Compiled by the authors

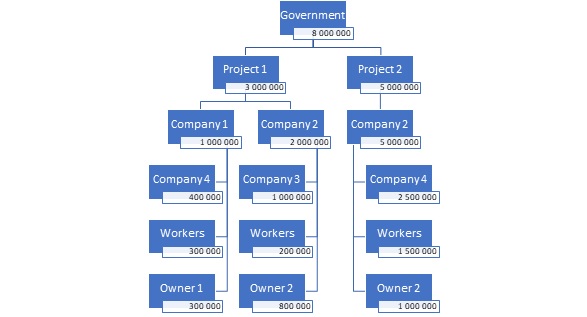

After that public investment blockchain will become the database of transactions of different projects. The flow of funds can later be analyzed using graph analysis methods. Figure 4 illustrates one simplified hypothetic example of state-funded projects graph that may derived from the data of our hypothetic public investment blockchain. Here government spends 8 000 000 currency unit to execute two projects, project 1 and project 2. Project 1 is executed by Company 1 and Company 2 for 3 000 000 currency units. company 1 buys goods and services from company 4 for 400 000 currency units, pays wage of 300 000 currency units to workers and owner 1 gets dividends from company 1 of 300 000 currency units, thus owner 1 has net profit margin of 30% from project 1. In project 1 Company 2 buys goods and services from company 3 for 1 000 000 currency units, pays wages of 200 000 currency units to workers and owner 2 gets dividends from this project of 800 000 currency units, thus owner 2 has net profit margin of 40%. Project 2 is executed by Company 2. In project 2 company 2 buys goods and services from company 4 for 2 500 000 currency units, pays wages of 1 500 000 to workers and dividends to owner 2 of 1 000 000 currency units. Here owner 2 has net profit margin of 20% from project 2. By examining the graph, we can ask some basic questions for example:

- Who owns company 3 and company 4?

- How efficient the transactions were?

- Were the alternative companies from which it was possible to buy goods and services cheaper?

- How efficient were projects in terms of execution costs? Should government fund such projects in future?

Figure 4. The example graph of state-funded projects

Source: Compiled by the authors

Blockchain technology as an investment project

Today there are various cryptocurrencies, the most well-known of them are Bitcoin, Ethereum, Tether USDt, Ripple, Dogecoin and others. In today's world of confrontational globalization (Bedianashvili, 2023; Papava, 2022) and currency wars, low- and middle-income countries can take advantage of this opportunity to build currency reserves at relatively low cost through blockchain. The main idea here is to issue a cryptocurrency at the level of a specific state or regional economic integration, which will have state support, place a certain amount of cryptocurrency in the genesis block, and if its value increases, it will be able to sell it, thus it will be able to gradually get out of the public debt or get new resources to finance large-scale projects. If we look at the increase in value, the price of cryptocurrency is affected by its support by states, convention and others, as a result, if we look at the market capitalization, successful cryptocurrencies often have a market capitalization worth tens and sometimes hundreds of billions of dollars, which is an attractive factor for creating a new cryptocurrency.

It is necessary to find out how cryptocurrency can be developed under different conditions by the state.

First, let's consider the case where one state is the creator of a cryptocurrency, but not its future controller. The state can place necessary amount of cryptocurrency in the blockchain genesis block, it may be the value in national currency of which will be the size (or more) of the debt (or the value of the project to be implemented) that the state wants to cover in the future. In this case, such a project will bring a one-time benefit to the state due to its creation of the new cryptocurrency. Here are two options:

- The amount of cryptocurrency issued is limited. In this case, the issuance of the currency will be controlled by an appropriate mechanism, be it the proof of work or proof of stack method, as a result, if the market capitalization reaches a certain level and is self-sufficient, then the state will sell the cryptocurrency in the genesis block, but this should not cause harm to other users and this should not become Ponzi scheme.

- The amount of cryptocurrency issued is unlimited. In this case, the issuance of cryptocurrency can be carried out by an algorithm that, without the intervention of the state or a specific user, will create a new cryptocurrency in the blockchain system after fulfilling certain conditions, for example, it can be a reward for validating a transaction, as is used in various cryptocurrencies (for example, in Ethereum). In this case, the market capitalization must grow faster than the amount of issued currency, so that this cryptocurrency does not devalue and the value of the cryptocurrency placed by the state in the genesis block does not decrease, but increases.

Consider the case where the state is the creator and controller of cryptocurrency. From the point of view of investors, when buying such cryptocurrency, there are risks that the issuer can at any time increase the supply of cryptocurrency, which will grow more than the market capitalization of this cryptocurrency, so its price will fall and investors will lose their property. Such a cryptocurrency could be Central Bank Digital Currency (CBDC).

At the level of international economic integration, several small states can create a cryptocurrency, and the genesis block will contain the required amount of cryptocurrency, which will be distributed accordingly based on the agreement of these states. If this currency will be issued in limited quantities, then as its value increases, so will the price of the quantity in the genesis block. In this case, simply at the level of an investment project, states can receive funds several times, and not borrow for the implementation of any project, because considering that so far, according to Forbes data of February 2024, the size of the entire cryptocurrency market is in the range of 2 trillion USD (https://www.forbes.com/digital-assets/crypto-prices/?sh=3c0b826a2478) and the capture of a large part of the market is quite difficult. When the market capitalization of the largest cryptocurrency by market capitalization, Bitcoin, in the same period is only 1 trillion US dollars, and the value of the second cryptocurrency, Ethereum, is 330 billion US dollars, then it is less possible to pay large debts in this way.

Using Blockchain technology for managing public debt by creating cryptocurrency is challenging. This technology at the same time creates possibilities with risks. There are risks for creators of cryptocurrency and for its users also. When country creates its cryptocurrency, it becomes its legal medium of exchange, this can cause different monetary fluctuations, which affects macroeconomic variables, that should be controlled by the government or that cryptocurrency may loss the status of medium of exchange, that means the losses for cryptocurrency investors. Creator should consider cybersecurity, which is challenging for the modern world. As a new medium of exchange, it will be required to implement various anti money laundering measures, which is also difficult.

Conclusion

To sum up, this paper reviewed possible blockchain technology applications for managing public debt. The first application that was reviewed was the efficiency increasing way by implementing blockchain to solve inefficiencies by traceability. This method can be used for gathering data about projects and assessing their efficiency. The second application of blockchain was cryptocurrency as an investment project. This may have benefits for receiving additional funds without borrowing, creating currency reserves with low costs and after that use that reserves to pay certain amount of debt. This method can also be used for international economic integration in the era of currency wars, where new global medium of exchange and reserve currency can be emerged. Both methods may create risks, because they involve integrating to financial system. The risks are:

- The risk of creating large business cycles caused by cryptocurrency fluctuations those may affect macroeconomic variables,

- Cyber security risks,

- The risk of losses for investors,

- Money laundering risks.

References

- Ahmed, A., (2018). How Blockchain Will Change HR Forever. https://www.forbes.com/sites/ashikahmed/ 2018/03/14/how-blockchain-will-change-hr-forever/# 6583597e727c.

- Akins, B. W., Charman J.,& Gordon, J. (2013). A Whole New World: Income Tax Considerations of the Bitcoin Economy (November 7, 2013). Pittsburgh Tax Review, Forthcoming, Available at SSRN: https://ssrn.com/abstract=2394738

- Barro, R. J. (1979). On the Determination of the Public Debt. Journal of Political Economy, 87(5), 940–971. http://www.jstor.org/stable/1833077

- Buffie, M. E. F., Berg, M. A., Portillo, R., Pattillo, M. C. A., & Zanna, L. F. (2012). Public investment, growth, and debt sustainability: Putting together the pieces. International Monetary Fund.

- Berg, A., Portillo, R., Yang, S. C. S., & Zanna, L. F. (2013). Public investment in resource-abundant developing countries. IMF Economic Review, 61(1), 92-129.

- Bedianashvili, G., Kokhreidze, G., (2023). Public Debt and Economic Growth in Small Countries under Contemporary Challenges. Ekonomisti, XIX(1), 98-110.

- Bedianashvili G. (2023). Macrosystemic Challenges of Uncertainty under the Conditions of Confrontational Globalization. Bulletin of the Georgian National Academy of Sciences, 17(2), 174-179.

- Casino, F.; Dasaklis, T.K.; Patsakis, C. A (2019). Systematic Literature Review of Blockchain-Based Applications: Current Status, Classification and Open Issues. Telemat. Inform., 36, 55–81.

- Charaia, V., Papava, V. (2021). Public Debt Increase Challenge under COVID-19 Pandemic Economic Crisis in the Caucasian Countries. Journal of Contemporary Issues in Business and Government Vol. 27, No. 3, 18-27. http://dx.doi.org/10.47750/cibg.2021.27.03.003

- Douglas W. A., Nathan J. B. & and Buckley, Ross P. B. (October 1, 2015). The Evolution of Fintech: A New Post-Crisis Paradigm? University of Hong Kong Faculty of Law Research Paper No. 2015/047, UNSW Law Research Paper No. 2016-62. http://dx.doi.org/10.2139/ssrn.2676553

- Kim ,H. M., Laskowski, M. (2016).Towards an Ontology-Driven Blockchain Design for Supply Chain Provenance, https://arxiv.org/abs/1610.02922

- Ko, V., Verity, A., (2016). Blockchain for the Humanitarian Sector - Future Opportunities. Report.

- McKinseyCompany (2016). Blockchain in insurance-opportunity or threat? https://www.mckinsey.com/industries/financial-services/our-insights/blockchain-ininsurance-opportunity-or-threat.

- MacDonald M. (21 September, 2022). Blockchain could bring a revolution in public financial management. OMFIF. https://www.omfif.org/2022/09/blockchain-could-bring-a-revolution-in-public-financial-management/

- Papava V. (2022). Pandemic, War and Economic Sanctions: From Turbulent to Confrontational Globalization. Eurasia Review, May 23. https://www.eurasiareview.com/23052022-pandemic-war-and-economic-sanctions-from-turbulent-to-confrontational-globalization-oped/?fbclid=IwAR1zLFJs1kUFJWgp6qRXRWhLOy2OWnWjwIVUjMwjphnjqs0OKoUQSi12Z4I

- Sichinava D., Maghradze M. (2023). Blockchain Technology, Cryptocurrency and Digital Currency: Current Situation and Key Challenges. Economics and Business, 4.

- Swan M. (2017). Anticipating the Economic Benefits of Blockchain. Technology Innovation Management Review . 7 (10), 6-13.